Imagine walking into a spacious, sun-drenched 1970s condo in the heart of downtown Calgary. It offers the kind of sprawling, column-free floor plan and "vintage gem" price point that feels like a steal. However, a savvy buyer must look beyond aesthetics and delve into the document package's technical jargon—specifically, the term "Post-Tension Cables" (PTC).

The line between a treasure and a financial nightmare can be thin. To navigate this decision, you must understand the structural realities, the financial complications, and your own risk tolerance.

The Basics

Post-tensioning involves steel strands embedded in concrete that are tensioned to provide structural strength. This allows for thinner slabs and open floor plans without heavy support columns. They were a staple of Calgary high-rises, parkades, and balconies from 1970 to 1980.

Bonded vs. Unbonded: The Critical Difference

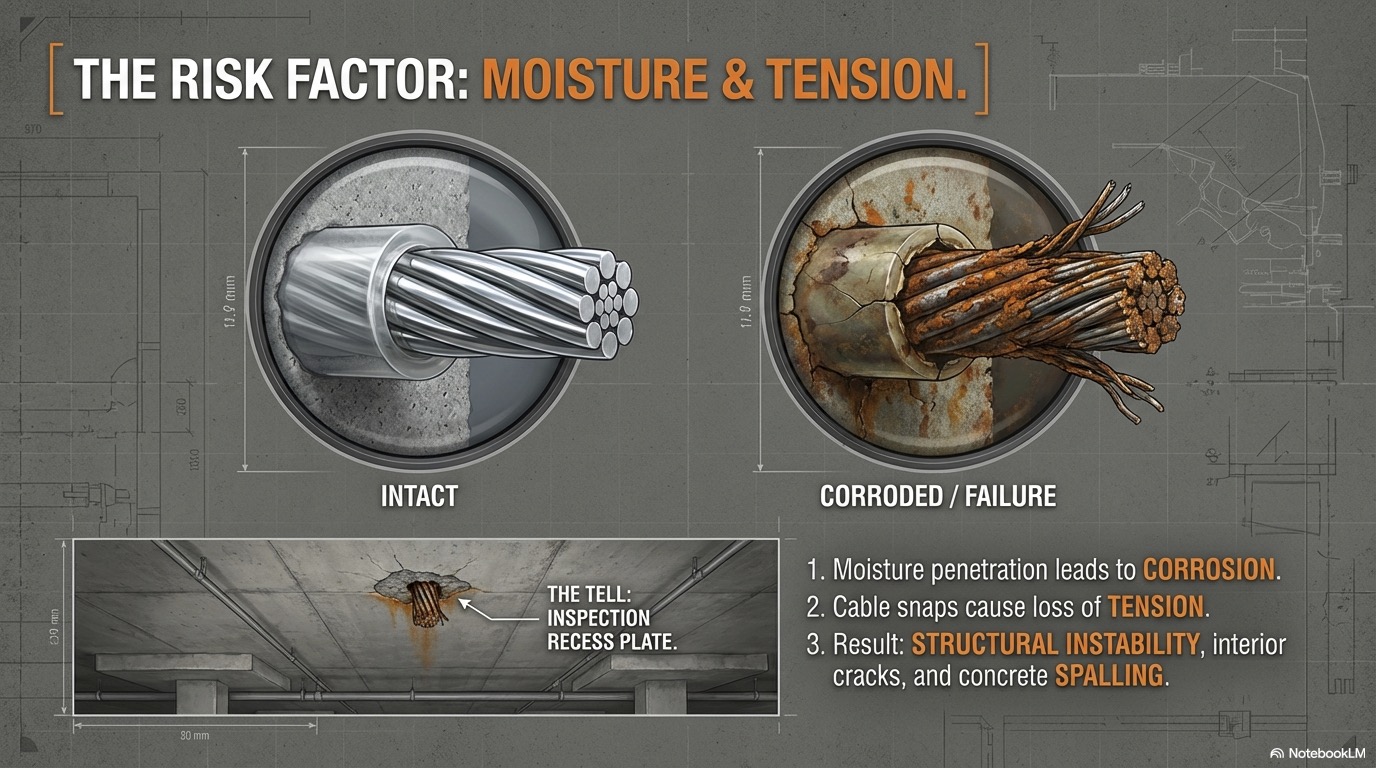

Unbonded (Residential Standard): Each strand is coated in grease and encased in a plastic sleeve. The tension is held entirely by steel anchors at the slab ends. While these can often be replaced if they fail, they are susceptible to moisture and salt—Calgary’s "Chinook cycles" of freezing and thawing make parkades and balconies higher risk zones for corrosion.

Bonded (Heavy Infrastructure): Strands are bundled in a duct and filled with cement grout. This creates a permanent bond along the entire length. While more durable and safer if cut, these cables cannot be replaced; a failure requires external structural reinforcement.

The Potential Problems

Because the PTC is embedded in the concrete, it is not easily visible or an easy fix, which could lead to high-stakes maintenance and replacement costs. Corrosion of the tendons is often caused by moisture/oxygen penetrating into sleeves, broken strands, loss of tension, damage from drilling/cutting, and anchor head deterioration.

Image created by Notebook LM.

The Maintenance

The City of Calgary’s Post-Tensioned Buildings Policy mandates rigorous monitoring. Corporations must hire specialized engineers (and potentially technologists, architects, and appraisers) for evaluations every one to five years. These engineers use inspection recess plates (small openings in the concrete slab) to assess the slab's overall condition and identify signs of rust, staining, cracking, tendon weakness, and anchor integrity. While tower slabs must be monitored, the most aggressive corrosion typically occurs in underground parkades, where de-icing salt and water infiltration are constant threats.

Inspections: Engineers use "inspection recess plates" to check for rust, staining, or cracking.

Parkades: While tower slabs must be monitored, the most aggressive corrosion typically occurs in underground parkades where de-icing salts and water infiltration are constant threats.

Potential Resale Challenges

Even if a building is declared structurally sound, PTC can be challenging for sellers due to a restricted lending pool and fewer buyers.

The Lender Gap: Currently, only about four lenders in the market will consider a PTC property, compared to the standard 20+.

Mandatory Insurance: Mortgage insurance is required regardless of your down payment. Even with 20% down, insurers such as CMHC must approve the building; Canada Guaranty will occasionally consider them, but Sagen currently refuses to underwrite them.

Insurance: Condos in buildings with PTC can be subject to higher premiums.

How to Spot PTC in the Paperwork

MLS listings disclose the existence of PTC. Once you have a conditional sale, review these specific documents:

Information Statement: This must legally state if PTCs exist and disclose any known structural deficiencies.

Engineer’s PTC Report: A technical assessment of the cables' condition and funding requirements for future repairs. A five-year cycle is common, but timelines vary based on PTC condition.

Reserve Fund Study: Confirms if the board has designated funds for the specialized inspections and remedial work these systems require.

Financial Statements: Review the Statement of Operations for actual expenditures on engineering monitoring and "Notes to the Financials" for any hidden liabilities or recent major repairs.

The Bottom Line

Before spending your time and energy viewing properties with PTC, confirm your lender and mortgage insurer's policies.

Buildings with PTCs introduce an additional layer of potential risk and expense. At the right price, you may be willing to accept the higher maintenance costs and the greater likelihood of challenges in future resale. On the other hand, with so many PTC-free condos available, you may decide that taking on a higher level of risk isn't worth the lower price.

If you and your lender are open to this material and construction, there may be an opportunity to secure a good deal, but keep in mind you will be on the other side of that transaction at some point.